Buying a house is a big deal. And where there’s a big deal, there’s usually a lot of misinformation. We talked with our preferred lenders and together we can expose the top myths when it comes to buying a house.

Myth #1: It’s all about the lowest interest rate.

In fact, the lowest rate does NOT equate to the lowest payment. There are a lot of variables when it comes to rate and overall packaging for your loan that results in payment. For example, you might choose to have lender paid mortgage insurance which will most often have a higher interest rate, but your monthly payment is lower. Example:

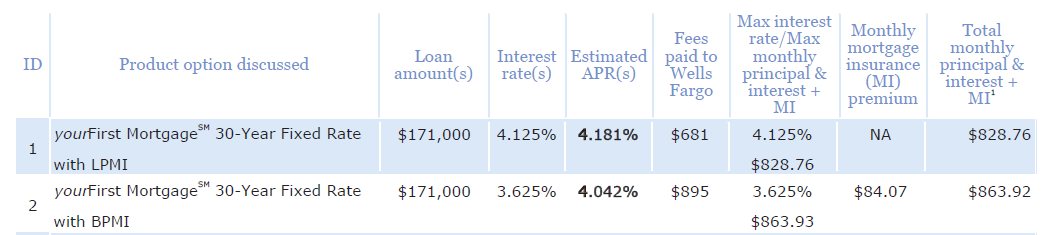

Let’s say you’re buying a house for $180,000. And, let’s say you’re going to put 5% ($9,000) down. Susan, at Wells Fargo, has put together some options for this example:

Option 1 has the lender paid mortgage insurance (LPMI) and the rate is $4.125%. That’s not really a terrible rate, but it IS higher than the 3.625% that you could get on a different program.

However, with the lender paid mortgage insurance – you don’t have that pesky mortgage insurance premium added to your monthly payment. So, your payment for principal and insurance (not including taxes or insurance) is $35.16 LESS than the payment at the lower rate.

It’s good to have options, right?

Using a rate to shop lenders also doesn’t help you choose a quality loan officer. Interest rates are a form of profit to the company. Typically, no one who is really good at what they do, is also the least expensive. For example, the prices at Wal-Mart are low, but usually Target is a better overall experience. But, if we’re comparing to quality – then I think Nordstrom beats both Wal-Mart and Target, hands down.

If I want to get the BEST steak, I’ll probably go to 801 Chophouse. But, if I want a more affordable steak then I might go to Applebee’s. The service, quality and overall experience are very different, aren’t they?

If we were doing a car reference I might say it’s the difference between a Hyundai vs. a BMW. But, I don’t really know cars that well, so I’ll just leave it at that.

The bottom line…

You get what you pay for, and it’s no different in the mortgage world. My team can tell you horror stories about loans that didn’t close on time. Loans that were denied right before they were scheduled to close because of something someone missed in the beginning. And many other similar stories with terrible outcomes.

When it’s your life possessions packed on a truck and your friends/relatives are coming into town to help, or the cable guy is scheduled for tv and internet installation, or something else equally inconvenient, you don’t want to find out that you “might” be closing on time – because your loan is in the hands of the lowest bidder. Just sayin’.

If you’d like to talk more about this, we’re here to help when you need us.